Sep 29, 2025

Flow Fatigue: Macro Headwinds Halt Rotation, Pressuring Key Support

Summary:

- U.S. Spot ETF flows were hit by major institutional liquidation: BTC shed ∼$897.6M and ETH recorded its largest weekly net outflow (∼$795.6M) since inception.

- The altcoin rally (TOTAL3) failed to sustain its ATH close, confirming the post-cut rotation is highly fragile without immediate inflow validation.

- Sticky US inflation (Core PCE) complicated the path for aggressive Fed easing, tightening the liquidity backdrop that drove the prior rally.

- Both majors are testing critical floors: ETH must defend the $3,850-4,000 range, while BTC's $104-105k structural shelf is now exposed.

- Breakouts failed across high-beta assets, with BNB slipping back under $1,000 and SOL stalling despite strong ETF narratives.

- Institutional productisation continues despite the sell-off, with the launch of the Staking ETH ETF and diversified index products (GDLC), deepening the long-term institutional rails.

- The imminent US Government shutdown deadline on Wednesday could delay key macro data (including the headline non-farm payroll) and complicate Fed decisions, even as markets price in a 90% Oct cut.

Rotation is alive but highly fragile

- Rotation Impulse Stalled: The post-Fed rate cut rotation impulse hit sharp resistance last week, evidenced by the TOTAL3 index failing to sustain its all-time high weekly close (chart below), underscoring the necessity of supportive flows for market breadth.

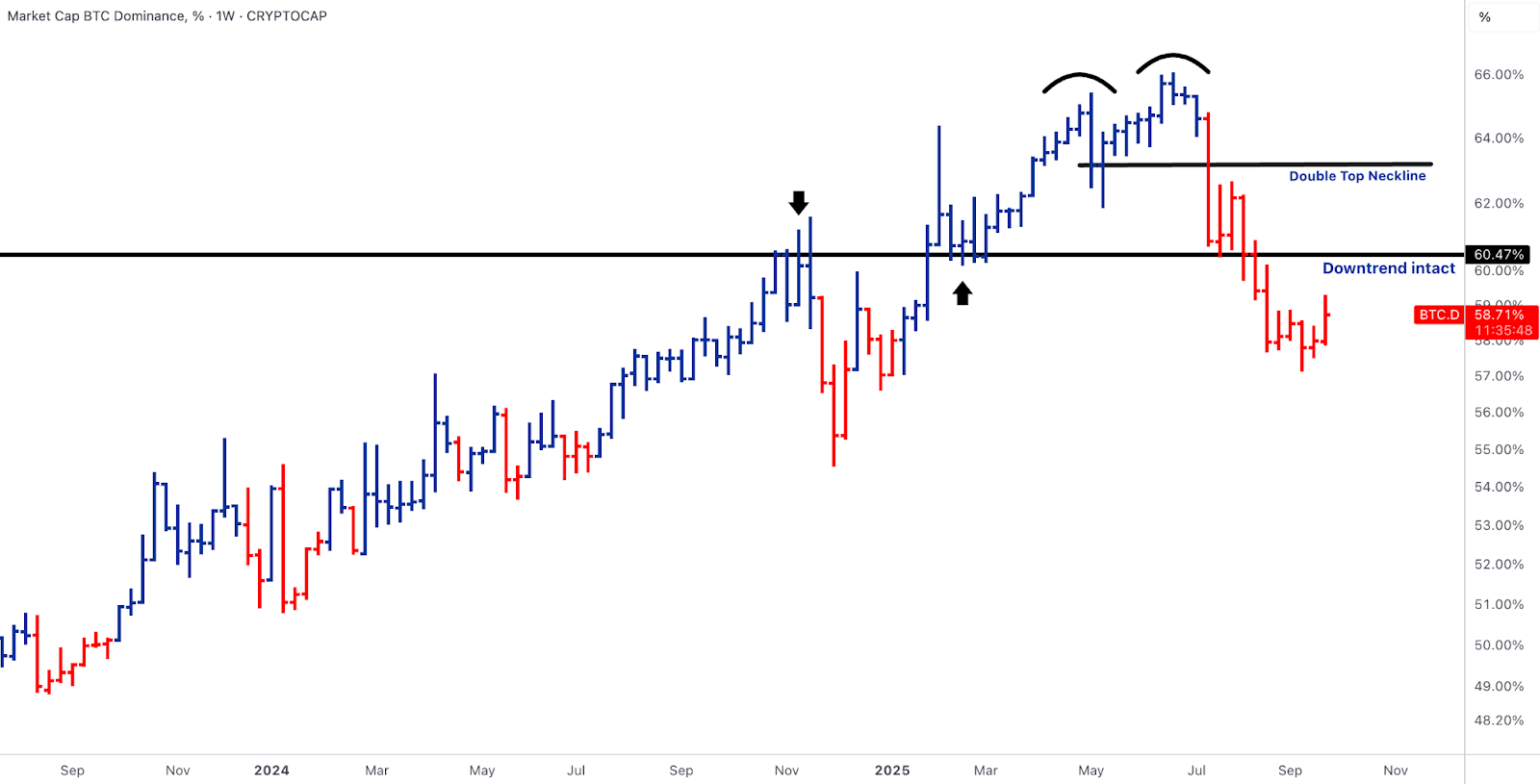

- Structural Alt Bias Remains (Fragile): BTC Dominance remains below the 60.5% neckline of its double-top breakdown, maintaining the structural bias toward alt outperformance, but recent alt leadership has been unconvincing.

- Alt Leadership Falters: Key high-beta assets showed fatigue: BNB slipped back under $1,000 after a failed breakout, and SOL stalled into overhead resistance despite a positive ETF narrative.

- Macro Capped Flows: Sticky August inflation data (PCE +0.3% m/m, core +0.2%) combined with strong personal income (+0.4%) and spending (+0.6%) blunted the post-cut rally.

- Fed Ambiguity: Strong macro data complicated expectations that the Fed's September rate cut signalled the start of a clean, sustained easing cycle.

- Sustained inflows are critical for validation, or leadership risks snapping back to Bitcoin.

BTC - Outflows stall the reclaim bid

- BTC’s structure deteriorated after failing to sustain above the 114-116k band, slipping back toward the ~109k handle (chart below).

- ETF flows flipped negative: spot BTC products shed ~$897.6M net over the week (Sept 22-26), reversing the prior week’s +$887M inflows. The pattern was consistent with defensive positioning ahead of the PCE release and equity market wobble.

- The distribution shows how pressure built into the inflation release: Mon saw -$363.1M, Tue -$103.8M, Wed +$241.0M, Thu -$253.4M, with the largest outflow of -$418.3M on Friday. With ETFs no longer providing the bid, BTC sits exposed. Support at 104-105k is the magnet zone, while the deeper 95-105k structural shelf remains intact below.

- Macro-wise, sticky core inflation and firm personal spending (+0.6% m/m) raise the bar for further Fed easing, tightening the liquidity backdrop that had enabled BTC’s September bounce. Unless ETF demand resumes, BTC risks drifting sideways-to-lower, leaving the burden of leadership with alts.

ETH - Outflows sharpen the test of 3,850-4,000

- ETH held the 3,850-4,000 defence zone (chart below) despite registering its largest net outflow week since inception across spot ETFs. Products bled heavily mid-week, with cumulative outflows reaching nearly ~$795.6M, a sharp reversal from last week’s inflows of $557M. Outflows were heaviest at the back end of the week: Thu -$251.2M, Fri -$248.4M, both record single-day prints.

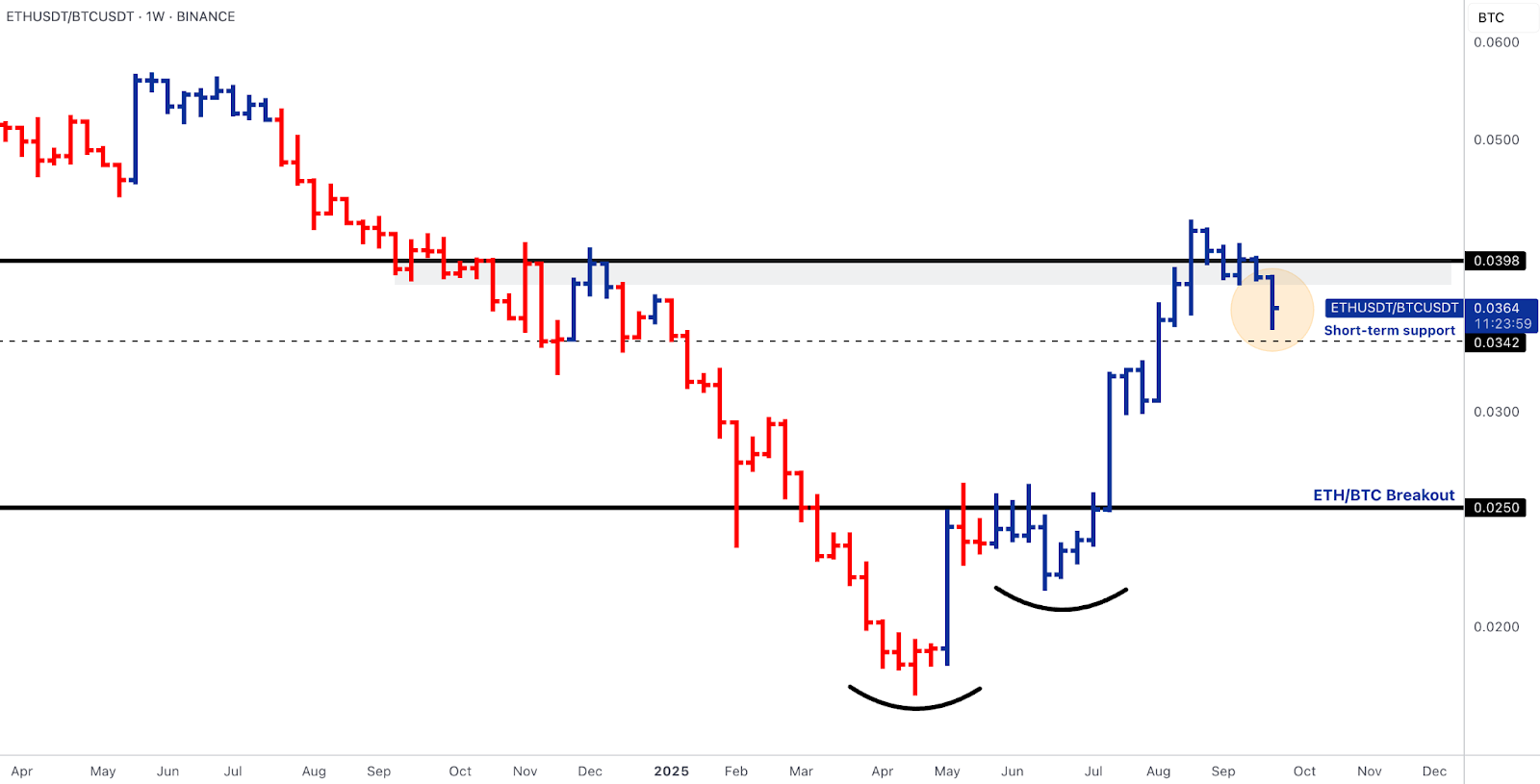

- On the chart, ETH/BTC slipped back toward 0.034-0.035 support, breaking short-term momentum but not yet invalidating the longer-term breakout. The flows are telling: allocators are reluctant to add risk into sticky inflation prints and Fed ambiguity, even as ETH’s structural rails expand.

- The launch of REX-Osprey’s staking ETH ETF is a milestone, bringing staking rewards inside the ETF wrapper, but it failed to offset broader outflows. Longer term, Bitmine’s accumulation of over 2% of the ETH supply reinforces staking’s centrality, but in the near term, ETH remains hostage to ETF flows.

- The technical hand-off zone (3,850-4,000) is pivotal: hold it, and ETH can re-challenge 4,550-4,630; lose it, and 3,400-3,600 comes back into play.

SOL & BNB - ETF anticipation vs breakout fatigue

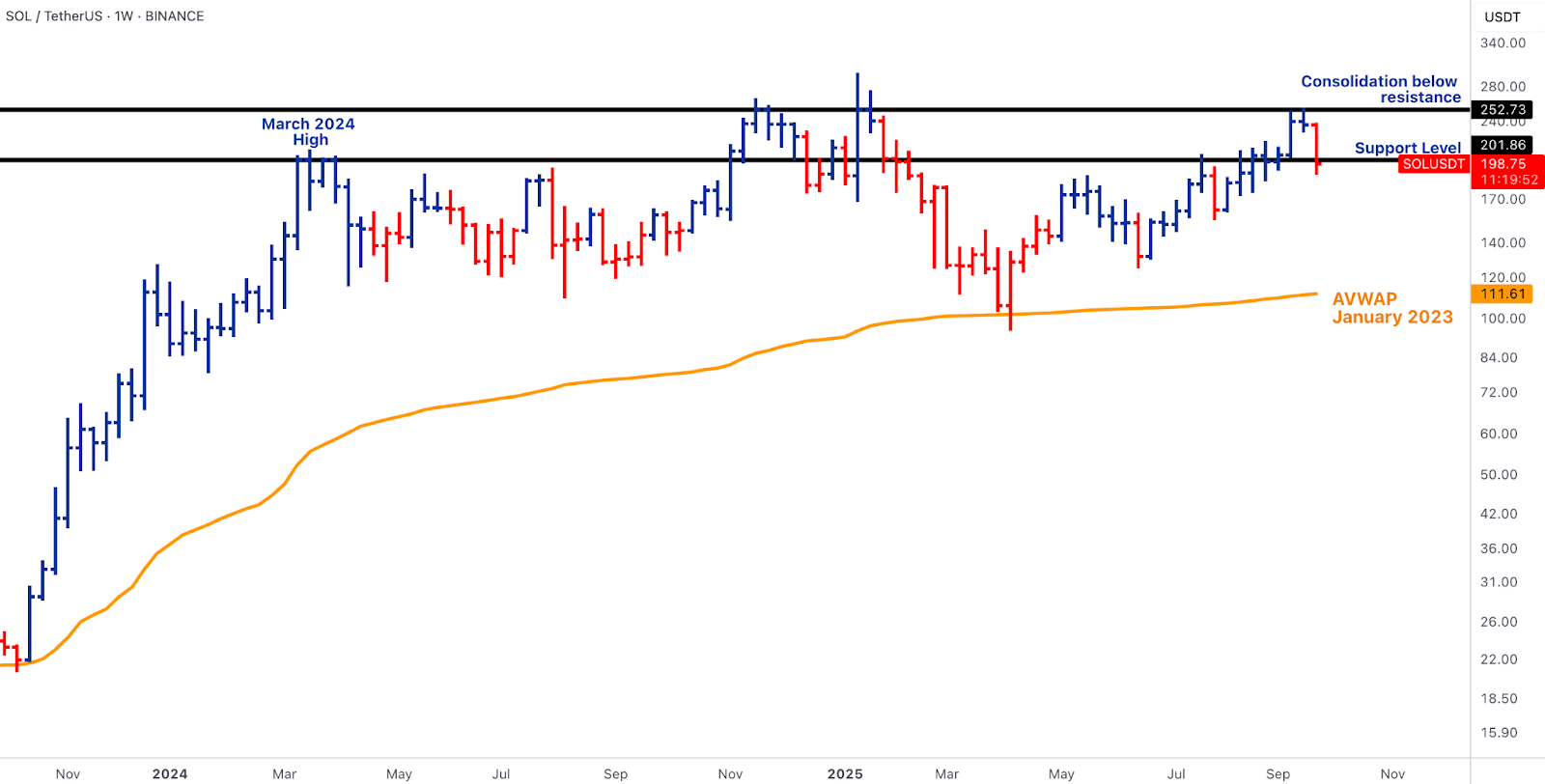

- SOL consolidated around 200-210 support after rejection near the 252-253 trigger zone (chart below). The narrative is constructive: amended filings suggest SOL ETFs could be weeks away, providing a direct US on-ramp for institutional demand.

- Balance-sheet sponsorship remains firm, but until confirmation, SOL’s tape looks tired after repeated failed pushes, although support held at the 200-210 zone, validating this as a structural base.

- Acceptance above $253 remains the unlock for a $275-285 measured move. BNB’s trajectory was emblematic of the week’s fragility. The token broke above $1,000 post-Fed only to slip back under, leaving a failed breakout on the tape.

- Unlike prior cycles, BNB’s fee capture and derivatives dominance give the move structural underpinning, but flows remain speculative at the margin. The failure to hold $1,000 narrows confidence in breadth, especially with BTC softening. Both SOL and BNB now serve as gauges: if they hold their defence zones, rotation persists; if they falter, BTC may re-centre leadership.

Emerging Rotation Leaders - selective catalysts

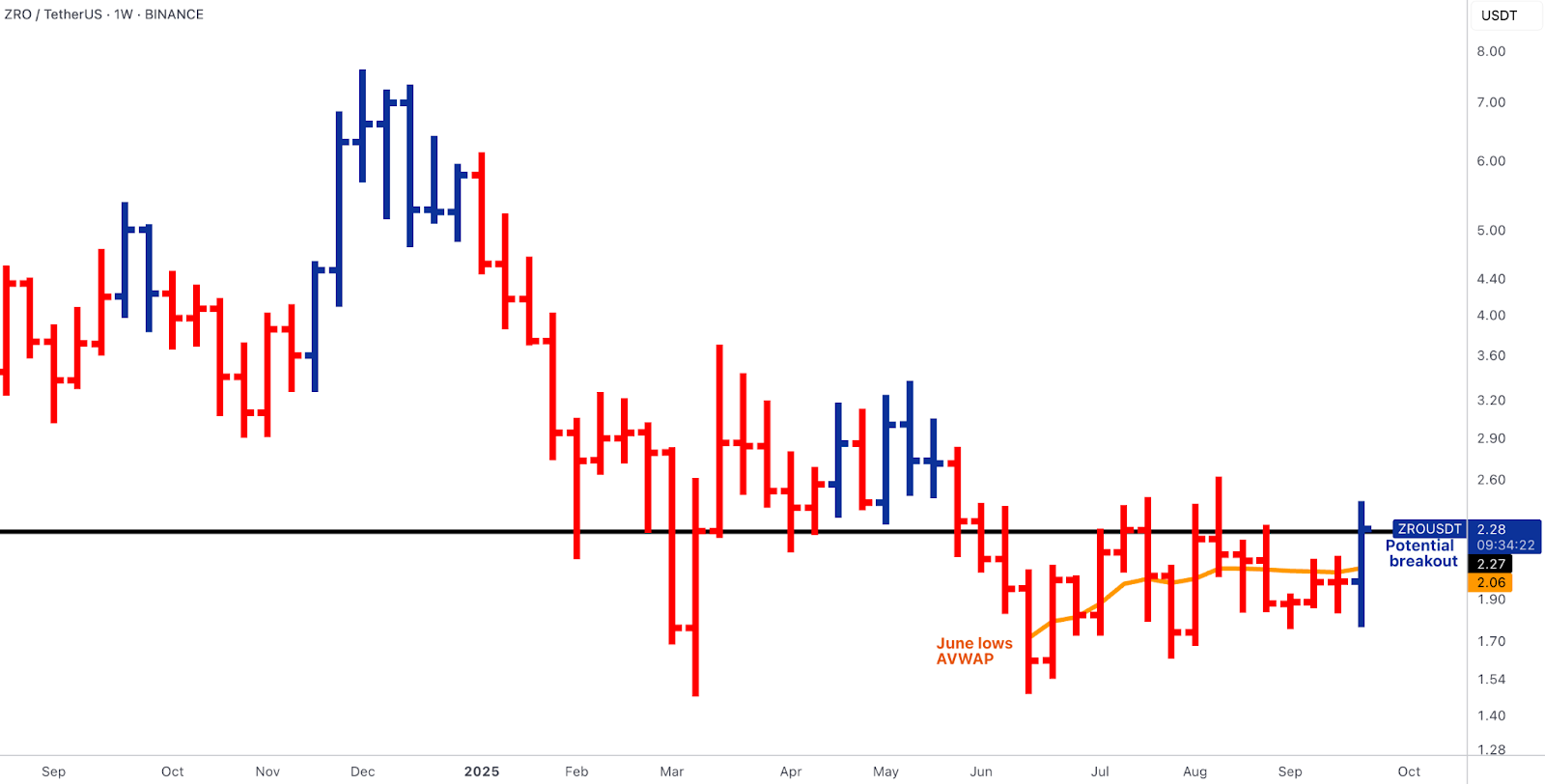

ZRO

- LayerZero absorbed its Sep 20 unlock (~25.7M, 8.5% supply) better than expected, with the STG merge consolidating bridging liquidity. Price pushed into a potential breakout above $2.25 (chart below). Reclaiming the June-low AVWAP also marks potential for outperformance here.

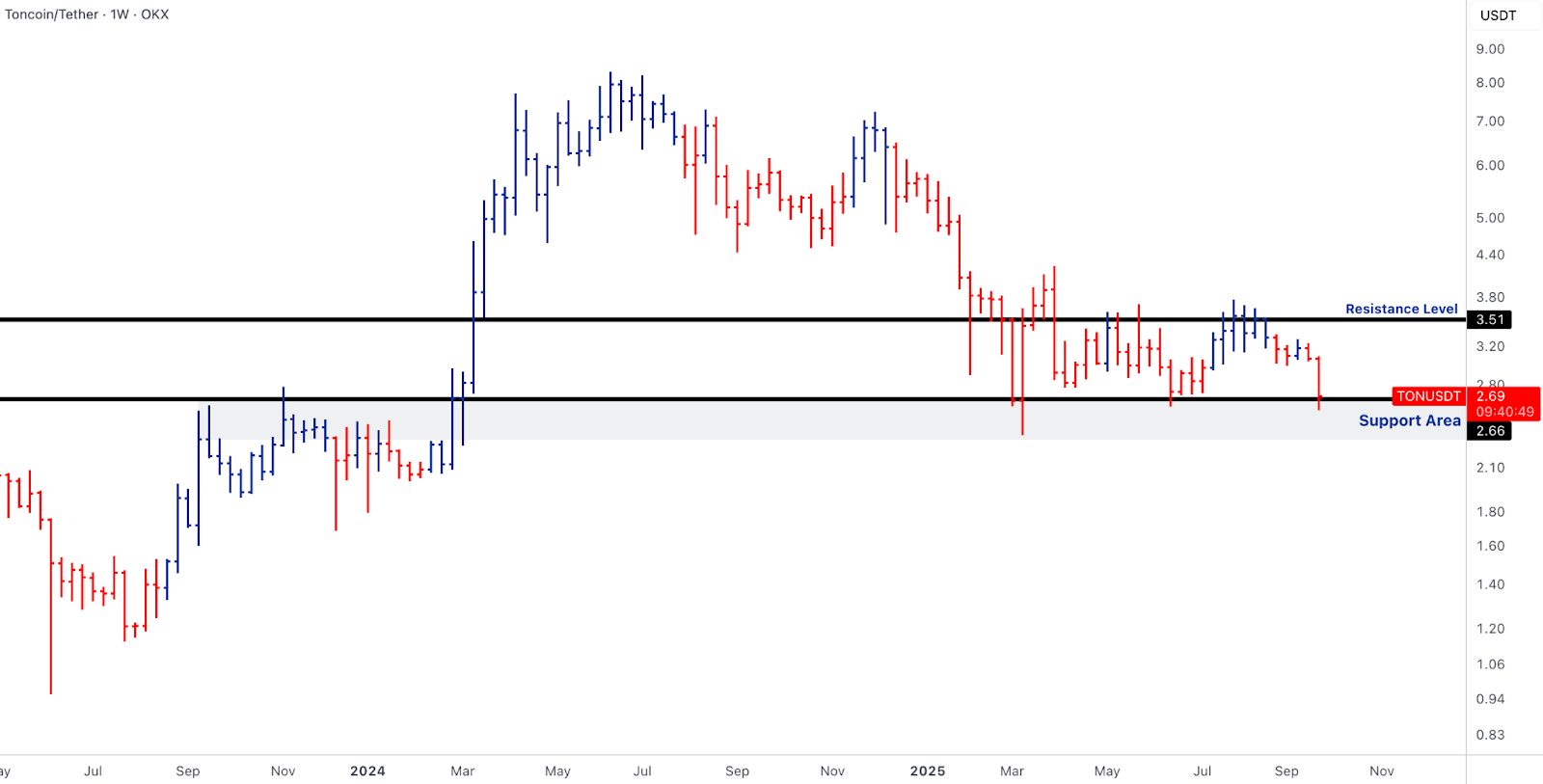

TON

- A Nasdaq-listed firm’s $30M TON purchase gave TON institutional sponsorship, but the price broke below $2.70 support (chart below). Unless it reclaims $3.00, the catalyst risks being dismissed as episodic. TON sits in the balance between strong narrative pull and weak chart structure.

AVAX

- The $550M treasury raise led by Scaramucci gave AVAX visibility. Price cleared $28.2 support and now tests the $30-33 resistance zone (chart below). Acceptance opens a path toward $38-40; rejection would leave it capped in mid-20s consolidation.

Plasma (XPL)

- The stablecoin Layer-1 launch with DeFi integrations drove XPL +79% WoW, putting it at the top of performance tables. Liquidity is thin, but the catalyst is real. Early days, but XPL is the week’s pure rotation expression.

Rails & Productisation - ETFs and stablecoins broaden institutional channels

- Last week saw distribution rails deepen on both the institutional and regulatory fronts. The REX-Osprey staking ETH ETF launched on Sep 25, embedding staking rewards within a US-regulated wrapper and marking the first mainstream bridge between on-chain economics and traditional fund structures.

- Bitwise filed for a Hyperliquid ETF, signalling that on-chain perpetuals are moving toward institutional packaging, while Grayscale introduced GDLC, the first spot-crypto index ETF, allowing allocators to access diversified exposure in a single instrument.

- In Europe, a consortium of banks announced a joint euro stablecoin initiative, extending the tokenisation drive into regulated digital cash issuance.

- Policy momentum kept pace, with the SEC floating an “innovation exemption” to accelerate crypto product approvals, and a US-UK task force announced to coordinate regulatory frameworks.

- Together, these rails highlight that product pipelines are not only broadening but also aligning more closely with regulatory structures, reinforcing crypto’s integration into mainstream financial plumbing.

Flow Fatigue vs. Technical Defence: Inflexion Point

- Last week confirmed that rotation is fragile, not entrenched. TOTAL3 breadth stalled, BTC and ETH ETFs printed heavy outflows (-$897.6M and -$795.6M respectively), and SOL/BNB both failed at breakout thresholds, yet support zones (BTC 104-105k, ETH 3,850-4,000, SOL 200-210, BNB ~$1,000) still hold.

- Rails deepened with new ETF products and euro stablecoin initiatives, anchoring liquidity beyond the tape. The path forward hinges on macro: a soft labour print could reignite flows and validate rotation, while sticky strength risks snapping leadership back to BTC.

Outlook for the week

- Investors are holding their breath for a possible US government shutdown. The greenback dropped while Treasuries rose on the back of that.

- Trump will meet with top Republican and Democratic leaders on Monday to discuss government funding prior to the pressing deadline.

- Without a deal, parts of the government would close on Wednesday. And a double whammy - this is also the date where new U.S. tariffs on heavy trucks, patented drugs and other items go into effect.

- If the US government were to go into shutdown, this would delay a slew of key macro data, including headline U.S. labour data (ISM PMIs, NFP).

- If there were no shutdown, markets would be looking for a sign of cooling that could reignite Fed rate-cut expectations and validate the altcoin rotation.

- However, if the shutdown goes beyond Fed meeting, the Fed will have to rely on private data to make the rate decision.

- Markets are now pricing in a 90% Fed rate cut in October, 68% of another cut in December.

- Several Fed and ECB governors are expected to speak this week.

Oops! Something went wrong while submitting the form.